The financial press reported a corporate partnership yesterday. Visa and OpenAI shook hands at the Visa Payments Forum in San Francisco on June 10, 2026. Mainstream headlines labeled it another standard artificial intelligence deal—a routine press release designed to capture short-term media attention.

That narrative completely misses the structural reality.

Visa has declared its operational intent to become the primary authorization and settlement layer for payments executed autonomously by software agents, not humans. This marks a profound architectural expansion for one of the most capital-efficient networks on the planet.

Under the framework of this agreement, Visa’s digital credentialing systems will integrate directly into OpenAI’s platform. This allows automated AI agents to execute multi-tier transactions within user-defined compliance guardrails—such as spending caps, authorized merchant scopes, and tokenized assurance metrics—without manual checkout friction.

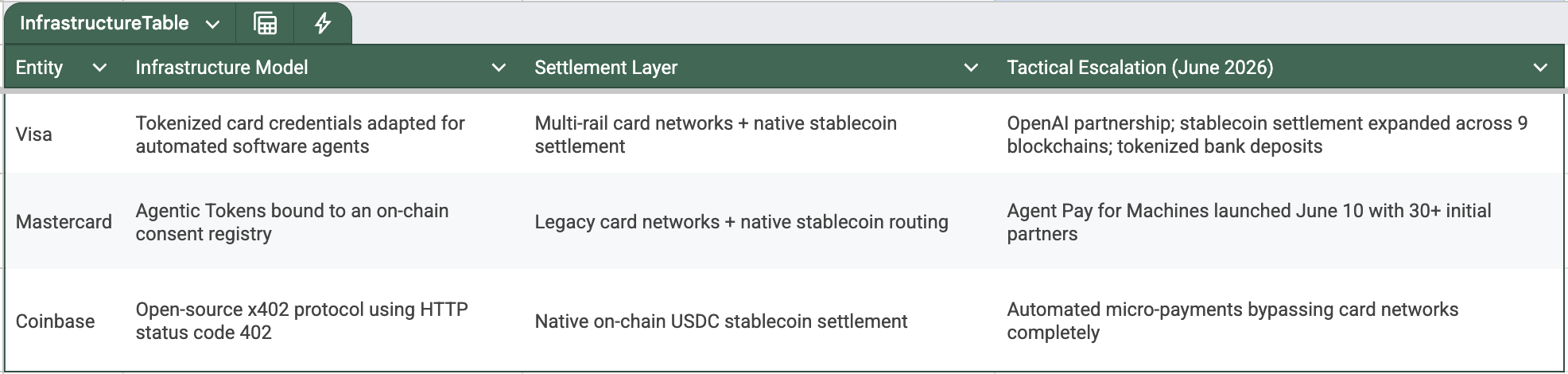

1. The Three-Front Infrastructure War: Visa, Mastercard, Coinbase

The public presentation claims these entities are simply competing for AI payment partnerships. The capital reality reveals three distinct structural models racing to establish the dominant tollgate for autonomous global commerce. Industry projections estimate the emerging agentic commerce market will reach $3 trillion to $5 trillion by 2030.

The battlefield as of June 2026 reveals a stark split between legacy network expansion and native blockchain architecture:

The structural divergence is absolute. Visa and Mastercard are stretching their legacy authorization moats into the agentic era by binding permissioning policies directly to proprietary tokens. Mastercard’s June 10 rollout of Agent Pay for Machines already spans 30 partners, integrating payment processors like Stripe and layer-1 networks like Solana.

Visa’s counter-strike focuses on volume and settlement versatility. The network’s internal stablecoin settlement system reached an annualized run rate of $7 billion as of March 2026—a 50% expansion quarter-over-quarter. By offering banks tokenized deposit technology alongside 160 live stablecoin card programs, Visa is positioning itself as the security layer on top of both fiat and digital rails.

2. The Balance Sheet Reality: High Margins Under Regulatory Siege

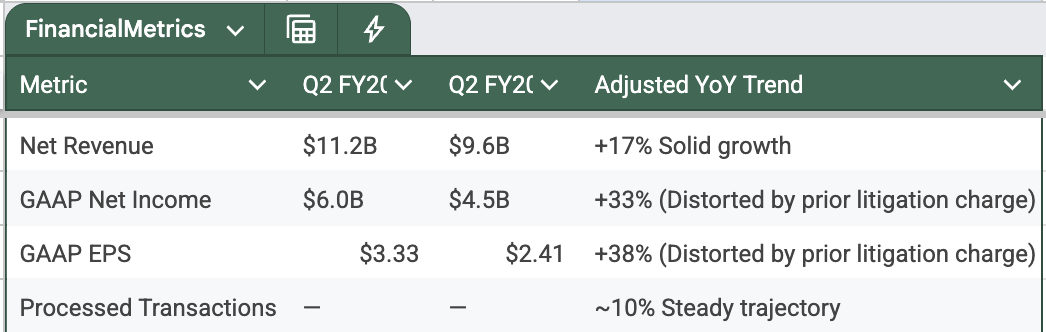

The core operational metrics of the business remain exceptionally strong, though institutional analysis requires looking past the manipulated year-over-year comparables.

Visa’s Q2 FY2026 financial reporting (quarter ended March 31, 2026) posted net revenue of $11.2 billion, a 17% increase year-over-year. GAAP net income hit $6.0 billion, showing a 33% expansion, while GAAP EPS climbed to $3.33.

However, the prior-year quarter included a significant $1 billion litigation provision. Adjusting for this baseline distortion reveals that while organic operational expansion remains highly robust, it is less dramatic than the headline figures suggest.

The model carries zero credit risk, requires minimal capital expenditure, and converts nearly half of net revenue directly into free cash flow. Yet, this high-yield operating leverage is facing its most significant legal threat in decades.

In the federal antitrust suit (United States v. Visa Inc., SDNY), the Department of Justice alleges that Visa maintains an illegal monopoly by using exclusionary pricing contracts to insulate its debit infrastructure. The DOJ asserts that Visa’s fee structures deliberately shield 75% of total U.S. debit volume from competitors.

Crucially, the U.S. District Court denied Visa’s motion to dismiss in full, ruling that the government adequately alleged substantial market foreclosure via exclusive loyalty schemes rather than standard price competition. The case is currently locked in active discovery, representing a structural variable that cannot be modeled with precision.

3. The Options Dislocation: Pricing the Spread

This regulatory cloud has created a unique valuation dislocation. While unusual options activity on June 9 showed a massive 87% spike in call option volume (64,086 contracts), the equity trades near $327. Independent valuation models place the high-probability entry zone at $290–$320, representing a trailing P/E of 25–28x—near Visa’s historical valuation troughs.

Furthermore, Visa debuted an upgraded tokenization system featuring a real-time token assurance signal. This architecture continuously updates a dynamic trust score across the entire lifecycle of a transaction, verifying credential setups and behavioral telemetry to eliminate systemic fraud before execution.

If this architecture holds, Visa secures its position as the universal toll collector, regardless of whether final settlement clears on legacy bank ledgers or public blockchains. This creates an ideal environment for sophisticated income-generation strategies on any macro-driven pullbacks.

4. The Sovereign Directive

For Individual Sovereigns managing capital for long-term financial autonomy, this infrastructure war dictates specific operational rules.

First, recognize that agentic commerce has transitioned from speculative venture capital into a multi-billion-dollar corporate production cycle. The multi-trillion-dollar market projections are secondary to the fact that Visa, Mastercard, and Coinbase are actively deploying massive engineering resources to lock down the future authorization layer.

Second, price the regulatory risk honestly. The DOJ antitrust case is moving through federal court. If the court eventually forces an unbundling of Visa’s debit routing contracts, it will permanently impair the network’s most profitable domestic revenue stream. Any capital allocated here must demand a strict margin of safety.

At $327, the equity reflects institutional optimism but fails to provide a sufficient discount to absorb potential legal fallout. Tactical patience remains an investor’s most lethal weapon. We do not chase the short-term option spikes. We watch the infrastructure buildout, wait for valuation to meet our defined parameters, and position our capital only when the math heavily favors our independent ledger.

Position accordingly.

🗳️ Sovereign Feedback: Your Input Dictates the Network

Bypassing the Human Wallet: How Visa and OpenAI Just Rewrote the Global Retail Moat

Visa is not launching features. It is repositioning its entire network architecture for AI agents.