The AI Disruption: Michael Burry’s $200M Palantir Trap Is Closing

PLTR hits its worst month on record as institutional allocators execute a structural exit.

THE 30-SECOND VERSION

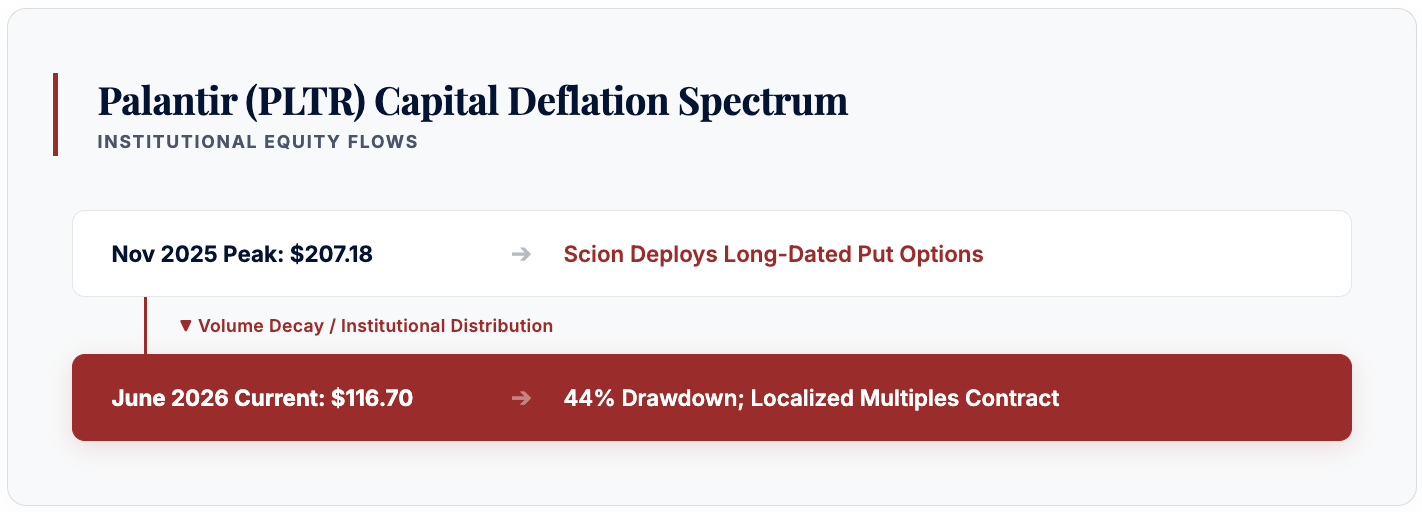

- The Palantir Unwind: Palantir (PLTR) dropped to $116.70, driving a brutal 25% collapse in June—the worst monthly performance in corporate history.

- Burry’s Victory: Michael Burry’s Scion Asset Management is up 44% since shorting the $207.18 peak.

- The Rotation Trap: While Cathie Wood’s ARK caught the falling knife with a $9.7 million dip-buy, the smart money is fleeing overhyped 100x P/E software and rotating directly into hard, sovereign infrastructure.

- Urgent: 5 Stocks You Should Sell Now (ad)

Welcome to your Wednesday Strategic Brief.

The grand enterprise software illusion is officially undergoing a forced re-pricing on the public tape, and the unhedged crowd is trapped in the exit bottleneck.

Palantir Technologies Inc. (PLTR) suffered another calculated 2.3% distribution drop on Tuesday, closing at $116.70 amid a broader, sector-wide technology contraction.

The asset has shed an astonishing 25% of its value in June alone and stands down 34% year-to-date. Let’s be entirely clear: this is not a routine market correction. This is the single worst monthly performance in Palantir's corporate history.

For the past twelve months, retail message boards and momentum buyers insisted that Alex Karp's enterprise software suite was an unassailable cash machine.

But having spent over two decades reviewing corporate balance sheets and procurement frameworks from the inside, I can tell you that the structural plumbing of global capital does not bend to marketing hype. Institutional desks are quietly winding down their exposure to over-multiplied SaaS architectures, leaving retail portfolios to absorb the downside velocity.

Here is the operational math behind the liquidation—and the strategic reality of the short-seller executing a textbook perimeter breach.

1. Structural Underhang: The Mechanics of Burry’s Short

The primary headwind restricting Palantir's cap table remains Scion Asset Management.

Michael Burry flag-planted his short position via put options when the stock achieved its record close of $207.18 on November 3, 2025. Since Burry identified that cyclical ceiling, PLTR has surrendered a staggering 44% of its total market capitalization.

In recent updates across his professional channels, Burry noted that the structural erosion of the asset is structurally intact:

"Palantir making a new lower low after an unimpressive low volume topping process... No sign of capitulation or exhaustion among sellers yet."

From an operational standpoint, Burry’s most lethal data point is the consistently declining trading volume over the last four quarters.

When a stock carves out fresh lower lows on drying volume, it indicates that institutional bidding has completely vanished. The smart money distributed its shares into retail bid pools months ago.

When you strip away the public relations layer, Palantir behaves less like a scalable software utility and more like a high-overhead professional services consultancy.

High stock-based compensation dilutes equity partners, while bloated corporate overhead—including excessive executive expenditure on private aviation—erodes structural margins. The market is finally waking up to the accounting mismatch.

2. The Great Rotation: The Premium Compression Cycle

Why is Palantir bleeding despite reporting nominally stable quarterly revenues? Because the macroeconomic layout has fundamentally shifted.

Institutional allocators are aggressively stripping capital out of software-as-a-service (SaaS) names trading at distorted valuations and rotating that liquidity directly into hard technology, energy infrastructure, and semiconductors.

When macro liquidity tightens, sophisticated capital stops paying a 100x price-to-earnings multiple for back-loaded growth promises.

If an enterprise does not generate immediate, defensive free cash flow or own physical, sovereign-backed assets, its multiple gets compressed by half. Palantir is simply the prime casualty of this systemic rotation.

3. Allocation Mismatch: Wood vs. Burry

As the software complex undergoes liquidation, we are witnessing an aggressive counter-move by legacy growth managers. Cathie Wood’s ARK Investment Management reversed its recent selling program on Tuesday, purchasing a $9.7 million block of PLTR shares on the decline.

ARK’s historical positioning reveals a volatile capital-reallocation loop:

- Nov 2025 – Jan 2026: ARK distributed over $60 million of PLTR stock near the absolute peak.

- April 2026: Wood re-entered the pool with a $10 million speculative buy.

- Tuesday: ARK injected an additional $9.7 million into the downward vector.

While ARK attempts to engineer a near-term technical bounce, the broader institutional tide is working against the position. In an environment defined by multiple contraction, one manager's emotional dip-buy simply serves as another institution's exit liquidity.

What they REALLY plan for your retirement

A devastating memo is quietly circulating in Washington.

It outlines a silent wealth transfer they call the "1776 Moment." The goal? To decouple intelligence from human labor and create a "useless class" of American workers.

The elites are quietly moving trillions into specific "choke point" monopolies while distracting you with political theater.

(ad)

4. Retail Psychology: The Illusory $100 Support

On retail messaging platforms, message volume for the PLTR ticker has surged 1,400% over the last 30 days. The retail community is reacting to the price action, and their internal conviction is beginning to crack.

According to internal sentiment tracking across major retail hubs:

- 50% of retail participants state they will refuse to allocate capital until the stock falls below $100—a psychological baseline last seen over a year ago.

- 34% of traders are actively attempting to front-run that level, placing speculative orders between $115 and $120.

This baseline suggests that the general public is no longer unconditionally buying every single red day. The crowd is moving its defensive parameters lower, confirming that true seller capitulation has not yet occurred. If the $115 horizontal level fails to hold, margin liquidations will likely trigger a rapid descent toward double digits.

The Bottom Line

Palantir has become a textbook case of asset-class rotation. On one side of the ledger, you have retail capital and momentum managers trying to catch a falling knife at $116.70, betting on a psychological psychological support level.

On the corporate side of the ledger, you have institutional desks quietly reallocating their capital out of high-multiple software entirely.

My operational directive has always been clear: never fight the volume profile. When institutional interest dries up during a structural breakdown, the professional allocator does not speculate on a bounce—he protects his capital perimeter and watches the liquidation from the sidelines.

The software premium is deflating, and capital is migrating toward hard, localized assets. Position your perimeter accordingly.

— Patrick Gibson, The Reclaimed Capitalist

You can also like:

- Trump’s Economic War Has Begun (ad)

- Germany turns to Ukrainian and Israeli start-ups for an alternative to US Tomahawk missiles (Business Insider)

- Nvidia pushes deeper into biomedical research (Yahoo Finance)

- This Startup is Growing 23X Faster than Nvidia (ad)

- Nvidia says AI’s water challenge is largely solved (Axios)

Disclaimer: This analysis is for educational purposes only and should not be considered investment advice. Always do your own research before making investment decisions.

Items marked with an asterisk (*) are promotional and help support this newsletter at no cost to readers.