The geopolitical and macroeconomic landscape altered drastically over the weekend. While retail participants are blindly chasing the early morning green screen, a self-directed sovereign investor views this morning’s optimism through a lens of cold, mathematical calculation. We have a highly compressed execution window ahead of us.

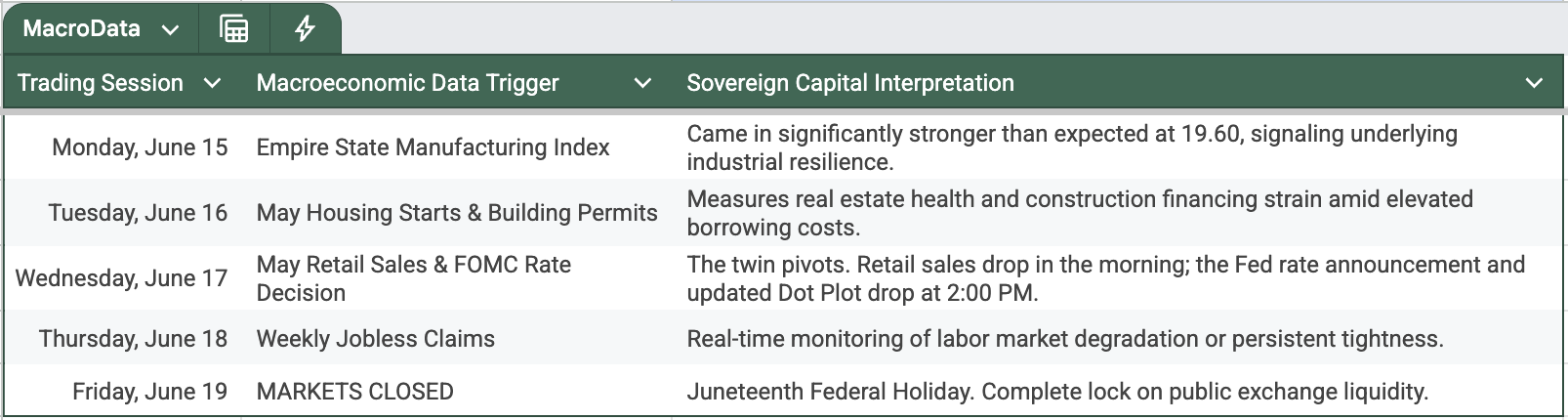

United States equity markets will be closed this Friday, June 19, 2026, in observance of the Juneteenth federal holiday. This packs all institutional flow adjustments, a critical retail print, and a historic Federal Reserve rate decision into a tight 72-hour operational corridor.

The weekend delivered a massive macro relief valve. Emerging reports confirm that the U.S. and Iran have established a tentative ceasefire framework to halt their three-month conflict, targeting a final pact signature this coming Friday in Switzerland. Crucially, the memorandum mandates an immediate unwinding of the naval blockade and a return to pre-war shipping volumes inside the strategic Strait of Hormuz within 30 days of signing. In immediate response, crude oil futures plummeted over 4%, with WTI settling down near $86.51 in late trading. This massive unwinding of energy-driven supply shocks has sparked an aggressive risk-on morning reaction, sending equity futures up over 1%.

1. The Capital Reality: Reconciling the 4.2% Inflation Hangover

The mainstream financial press is framing this morning’s index pop as an unencumbered green light for equity accumulation. The underlying data reveals a far more complex structural landscape that demands strict portfolio discipline.

Last week’s data digestion was heavily colored by the Consumer Price Index (CPI) print, which accelerated to a hot, three-year high of 4.2%. While the sudden weekend collapse in crude oil will eventually filter through to cool wholesale price distributions, the near-term reality of sticky, structural inflation remains a severe administrative drag on asset multiples.

This sticky baseline has driven an aggressive divergence in market architecture. We are witnessing a clear K-shaped consumer spending pattern. High-income brackets continue to absorb elevated financing costs, while middle-to-lower tranches are aggressively tightening their belts on big-ticket discretionary items, shifting allocations exclusively toward essential consumer staples and lower-tier essential services.

2. The Strategic Catalyst: Warsh’s Baptism by Fire

The absolute main event of this compressed week arrives on Wednesday, June 17, marking the first Federal Open Market Committee (FOMC) rate decision under the leadership of the newly appointed Fed Chair, Kevin Warsh.

The institutional framework for the next 72 hours outlines a highly concentrated macro calendar:

CME FedWatch metrics currently assign a 99% probability that the FOMC will hold interest rates static within the 3.50% to 3.75% band. Because the rate hold is a mathematical consensus, institutional desks will be hyper-focused on the fresh “dot plot” interest rate projections and the specific tone of Warsh’s debut press conference. The central question is whether the 4.2% CPI print will force Warsh to debut with an aggressively hawkish, “higher-for-longer” policy stance that caps corporate equity multiples through late Q3.

3. Corporate Earnings: The Operational Proxies

While we are past the standard seasonal earnings peak, three key corporate bellwethers report this week. These reports will serve as direct operational proxies to verify the health of the macroeconomic transmission belt:

- Lennar (LEN): Provides direct balance sheet insight into the housing market’s ability to sustain volume under elevated mortgage rates and structural inventory deficits.

- Kroger (KR): Serves as a vital diagnostic tool for the consumer staple layer, revealing whether margin expansion is sustaining or if raw grocery inflation is finally triggering severe consumer volume resistance.

- FedEx (FDX): The ultimate global logistics and shipping proxy. This print will directly validate or invalidate the World Bank’s revised 2026 global growth forecast, which was recently cut to a muted 2.5% due to prolonged conflict-related supply chain drag.

4. The Sovereign Directive

For Individual Sovereigns focused on long-term capital preservation, this compressed week requires absolute emotional insulation from morning headline pops.

First, do not chase the open-market index momentum today. The early surge in airlines, cruise lines, and tech futures is a mechanical reaction to lower near-term fuel overhead and the unwinding of geopolitical risk premiums. However, a market jumping on headline hopes before an unconfirmed international signature is highly volatile. The Hormuz naval blockade remains legally intact until the physical ink dries in Switzerland this Friday.

Second, utilize this temporary surge in implied volatility to re-balance your active risk parameters. The explosive morning rally provides an optimal window to write out-of-the-money covered calls against overextended technology or discretionary positions. This allows you to convert the media hype into a guaranteed premium—your Sovereign Paycheck ahead of Wednesday’s high-stakes Fed decision.

Third, maintain a defensive positioning matrix until Warsh delivers the dot plot. If the new Fed Chair takes an uncompromising stance on the 4.2% CPI data, the market’s early week optimism will erase violently. Let the retail crowd gamble on the exact wording of the FOMC press release. Our operational protocol is to collect premium cash flows from the structural noise, maintain an elevated cash-secured reserve, and deploy active buying power only when the macroeconomic numbers—not the weekend headlines—support a clear margin of safety.

Position accordingly.

🗳️ Sovereign Feedback: Your Input Dictates the Network

The Monday Macro Re-Anchor: Warsh’s Debut, Hormuz Relief, and the Four-Day Execution Plan

Inside the K-shaped consumer pivot and the options strategy to front-run the new Fed Chair's dot plot.