I have tracked this exact pattern across multiple market cycles. A dominant tech platform grows headline revenue, adjusts forward guidance metrics, and aggressively buys private competitors to defend its perimeter. Yet, the equity plummets 34% in six months while sell-side analysts blindly maintain “Moderate Buy” ratings with mathematically impossible upside targets.

The financial press calls this a temporary sentiment problem. I call it a permanent, structural repricing that mainstream media is fundamentally unequipped to diagnose.

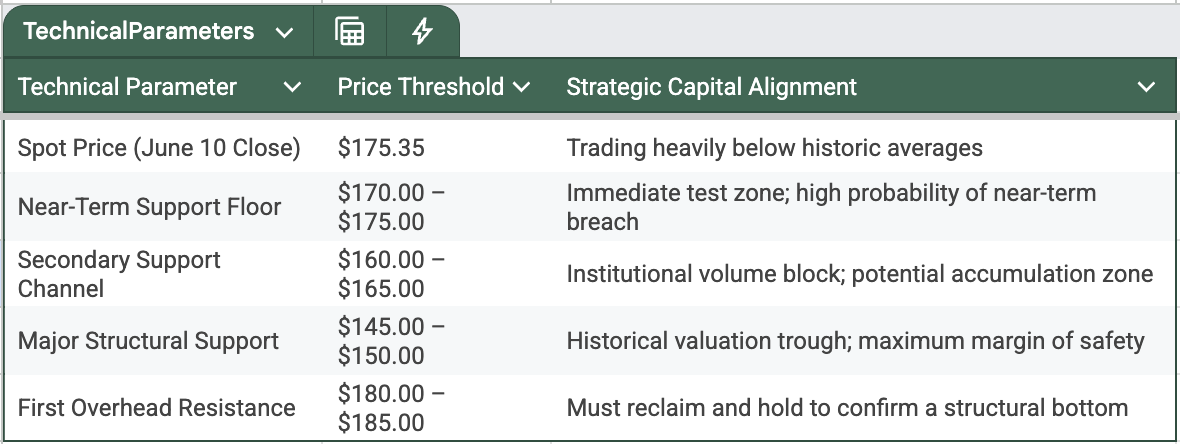

Salesforce closed at $175.35 on June 10, completing a six-day losing streak that erased roughly $30 billion in market capitalization. The stock is now down more than 33% year-to-date, making it one of the most aggressive capital destruction events in large-cap software this year. While the retail crowd buys the narrative of a brief rotation, the underlying institutional flow data reveals a planned capital exodus by the very firms that engineered these multi-year highs.

1. The SaaSpocalypse: Multiples Hit a Decade Low

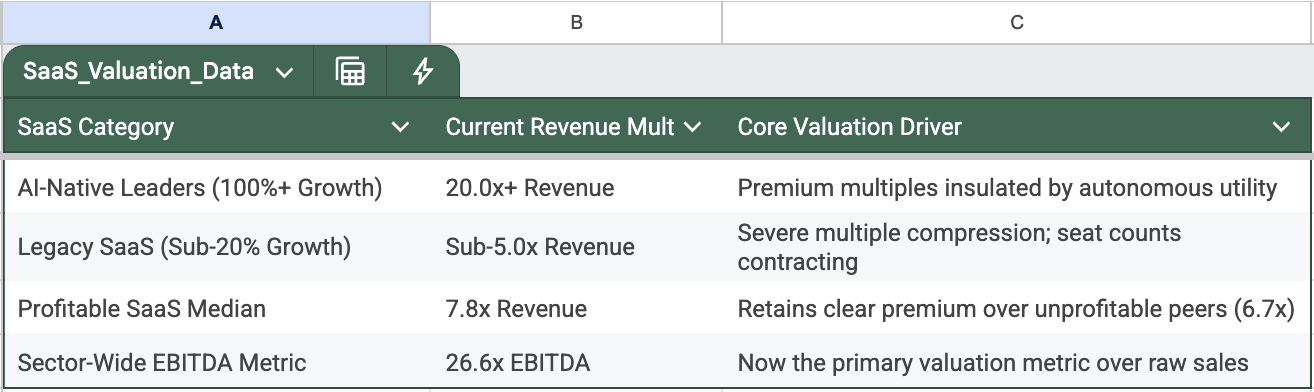

The ongoing sector liquidation, internally dubbed the “SaaSpocalypse,” recently vaporized a staggering $285 billion from global software stocks following the maturation of advanced, autonomous AI agent platforms. The median enterprise-value-to-revenue multiple for public SaaS firms compressed violently to 3.4x—marking the absolute lowest valuation floor since data tracking modernized in 2015.

The enterprise software market has split with surgical precision, forcing a complete breakdown of the legacy per-seat licensing paradigm:

Salesforce is caught directly in this transition zone. While trailing twelve-month (TTM) revenue stands at $42.22 billion with year-over-year expansion at 8.7%, its valuation metrics—a P/E of 24.48 and a P/S of 4.37—confirm that Wall Street will no longer pay an infrastructure premium for single-digit growth. To protect its perimeter, Salesforce executed emergency acquisitions of Own Company for $1.9 billion and Contentful for roughly $1.5 billion.

These transactions were executed at devastating 43% to 65% discounts relative to their peak private valuations. When an industry giant builds its growth narrative on distressed asset fire-sales, it signals that the legacy core engine is stalling.

2. The Capital Reality: Historic Institutional Tech Outflows

The establishment media wants retail investors to believe that this volatility is a psychological reaction to near-term AI adoption timelines. The underlying money flow metrics expose this as a total fiction.

Bank of America’s latest institutional flow data confirms that clients executed a record net liquidation of $14.2 billion in U.S. equities in a single week, with technology stocks absorbing the absolute bulk of the selling pressure. This historic technology cash extraction represents the largest single sector outflow tracked since 2008. The liquidation cascade was driven entirely by institutional desks dumping large-cap tech, while private client buybacks simultaneously collapsed to historic lows.

This is not a mood swing; it is a mechanical re-allocation of capital away from over-leveraged business models. The primary catalyst was a massive macroeconomic jobs print that pushed the 10-year Treasury yield up to 4.54%. Higher capital costs dramatically increase the cost of enterprise data center deployment, rendering legacy software cash flows less valuable when discounted back to current dollar terms. The largest players on the Street are unwinding their positions because the mathematical floor has shifted.

3. The Structural Threat: The End of the Per-Seat License

The boardroom narrative focuses heavily on the deployment of Agentforce, claiming that combined annualized recurring revenue (ARR) alongside Data 360 has crossed the $1.4 billion milestone. While management leverages this to raise fiscal 2026 revenue guidance to $41.55 billion, the numbers hide a fatal structural vulnerability.

This $1.4 billion ARR layer represents a minor 3.3% of Salesforce’s total revenue footprint, and its core generative engine—the Agentforce Content Agent—remains locked in a pilot phase. The existential threat to Salesforce is not a traditional competitor; it is the fundamental obsolescence of the per-seat software model.

For two decades, enterprise software scaled by charging a flat fee per human employee user license. However, agentic AI systems are capable of executing autonomous workflows at a fraction of human operational timelines.

As corporate clients realize an AI agent can execute the workload of entire departments, enterprise seat counts will contract permanently. If a company can build an internal alternative or run an external agent for a flat token fee, it will refuse to renew multi-million-dollar CRM software licenses. Salesforce is trapped in an architectural paradox: it must build the very agentic tools that are structurally designed to eat its legacy revenue streams.

4. The Sovereign Directive

For Individual Sovereigns managing capital for long-term financial autonomy, this sector demolition dictates precise strategic positioning.

First, recognize that the SaaS repricing event is not a temporary market correction. It is an industrial reset. The legacy software licensing model is entering a phase of structural obsolescence. Any capital positioned inside this sector must be valued based on realized free cash flow multiples, not hyper-inflated revenue projections.

Second, map out the technical support lines with absolute calculation before deploying a single dollar of risk capital. Salesforce is currently trading under every major moving average, confirming intense institutional distribution:

Third, exercise defensive patience. The stock is hovering near its 52-week low, and short-term quantitative modeling projects a continued negative path down toward the $160.00 threshold. Buying a falling large-cap knife based on historical brand dominance is a retail trap.

Let the institutional liquidation run its course. True capital reclamation requires waiting for these platforms to permanently adjust their pricing models to an agentic reality before exposing your independent ledger to their balance sheet volatility.

🗳️ Sovereign Feedback: Your Input Dictates the Network

The $30 Billion Salesforce Flush: Pricing the Collapse of Per-Seat Licensing

Institutional tech selling hit levels not seen since 2008. Your capital directive inside.