Instead of succumbing to the media euphoria surrounding NASA's recent moon base blueprint, we are executing a cold, calculated audit of the sector. The space agency has distributed hundreds of millions of dollars in contracts across four enterprises—Jeff Bezos’ Blue Origin, Astrolab, Lunar Outpost, and Firefly Aerospace. The operational objective is to deliver landers, rovers, and drones to the lunar south pole by 2028.

To the retail investor, this appears to be the dawn of a new technological frontier. To us, it represents a massive corporate debt cycle that introduces profound inefficiencies into the public supply chain. Our directive is simple: strip away the public relations noise and dissect the raw financial architecture of these contracts.

1. Contract Anatomy: Fixed-Price vs. Structural Inflation

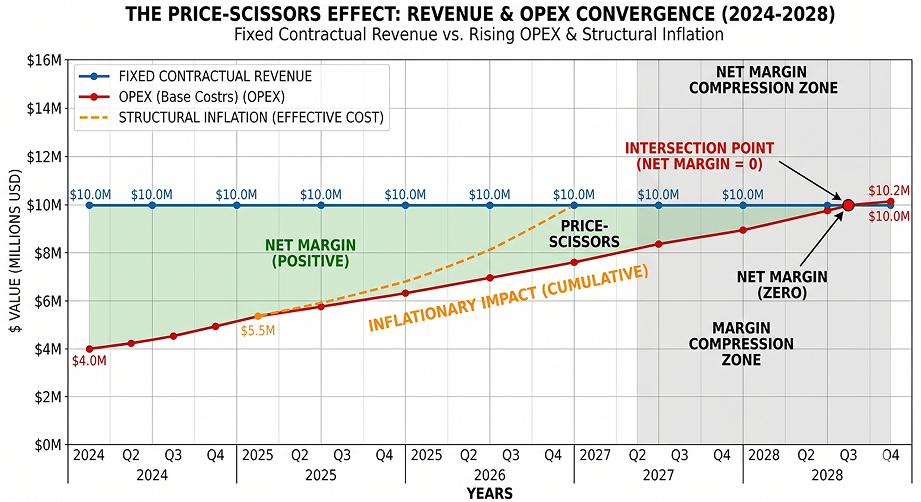

The primary structural vulnerability within the latest NASA awards lies in their legal and financial underwriting. The vast majority of these state defense and aerospace allocations are structured strictly as Fixed-Price Contracts.

- Risk Transfer: NASA caps its multi-million dollar capital injections years in advance. Consequently, all operational execution risks—ranging from supply chain bottlenecks to rare-earth material shortages and escalating labor costs—are shifted entirely onto the corporate balance sheets.

- The 2028 Horizon: Hardware delivery is benchmarked for 2028. Under high structural inflation, the operating margins calculated in 2026 will be systemically eroded by the time final assembly occurs.

- Capital Expenditures ($CAPEX$): Entities like Firefly and the legacy suppliers partnering with Blue Origin require immediate, intensive working capital to scale up production capacity.

When corporations sign these long-term commitments, they are forced to tap the debt markets. Crucially, they must do so under highly restrictive macroeconomic credit conditions.

2. Leverage and the Administrative Drag of Aerospace Giants

To absorb these multi-million dollar mandates, public aerospace and defense components utilize intensive financial leverage. They issue corporate bonds or open credit facilities backed entirely by projected government disbursements.

Behind the sleek investor decks showcasing lunar terrain vehicles lies a dangerous operational reality. Management routinely weaponizes these long-term state backstops as a smokescreen to mask profound administrative drag and decaying core profitability from activist shareholders.

They present a guaranteed revenue backlog spanning 5 to 7 years to the public. What they omit is that the debt service required to fund the initial research and development aggressively cannibalizes net income in the current quarter. This is classic boardroom metric management bordering on balance sheet manipulation.

3. Tactical Analysis: Locating the Structural Inefficiencies

We do not trade on sentiment, nor do we blindly accumulate aerospace equities for the long term. We isolate the specific operational zones where actual cash flows diverge from market expectations, creating elevated implied volatility ($IV$).

Institutional market makers are fully aware of these underlying strains. They will wait for retail capital to bid up equity valuations on positive testing headlines, then systematically harvest the premium or hedge their exposure using advanced derivative structures. We will position ourselves directly counter to this retail liquidation cycle.

4. The Tactical Strike Plan: Extracting Premium from Volatility

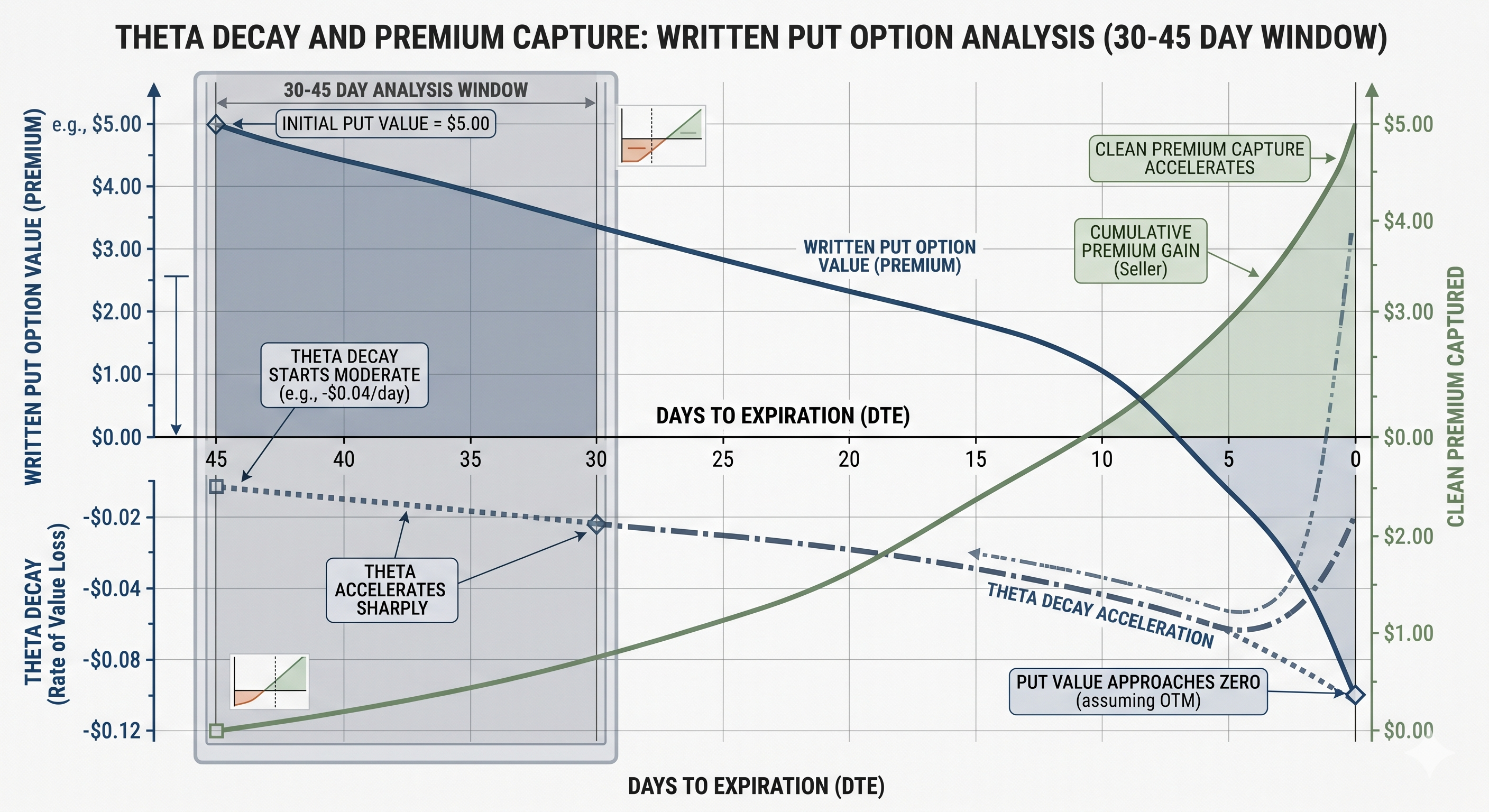

Rather than assuming unhedged directional equity risk within a capital-intensive sector, we execute a mathematically rigorous options strategy. The elevated uncertainty surrounding the 2028 execution deadlines artificially inflates options pricing. We treat this volatility as a pure income-generating asset.

- Cash-Secured Puts: We isolate highly liquid, large-cap aerospace and defense ETFs or robust, systemically vital component suppliers embedded in the supply chain. By writing puts 15% below the current spot price with a 30-to-45-day horizon, we extract immediate upfront premium from panicked market participants buying downside insurance.

- Position Management: In the event of a broad market correction where we are assigned shares, we immediately pivot to writing covered calls against the underlying position. This mechanics-driven rotation compounds our yield and systematically drives down our cost basis, completely detached from whether a drone launches on schedule or faces administrative delays.

5. The Sovereign Directive

A multi-million dollar lunar contract is not a structural guarantee of equity appreciation. It is a lagging indicator that an enterprise is entering a phase of severe operational strain and debt expansion.

Institutional capital evaluates these entities on a trailing Free Cash Flow ($FCF$) basis and the absolute health of the balance sheet, while retail participants chase superficial headlines regarding the lunar south pole. Our strategy is to remain firmly anchored to the math of decaying assets. Let the corporations shoulder the execution risks of 2028; our mandate is to extract the options premium here and now.

The Tactical Strike Plan: Trade NASA’s $20B Cash

How space giants use state contracts to hide decay.