Today, the very debt structures that funded endless corporate mergers and aggressive restructurings are fracturing rapidly. According to May reports from Fitch Ratings, U.S. private credit defaults hit a record 6% in April. Across the board last year, borrowers backed by private credit posted a 9.2% default rate. As a direct result, Blue Owl Capital froze redemptions on its main fund, and BlackRock has strictly capped investor withdrawals at 5%, despite redemption requests reaching 9.3%.

The same corporations that executed these efficiency optimizations are now locking the gates on their own investors. Meanwhile, the dividend yield of the S&P 500 has degraded to roughly 1%—a structural low not seen since the 19th century. If you are counting on passive index funds to fund your retirement, or if you have left your capital locked inside these gated institutional structures, your wealth is at risk. This memorandum delivers a pragmatic counter-strategy: a self-directed covered call overlay on equities with maximum financial durability. This framework is engineered to generate a baseline yield of 10%+ per annum, remaining fully under your execution and control.

1. The Corporate Debt Fracture: Why Your Income Must Be Self-Directed

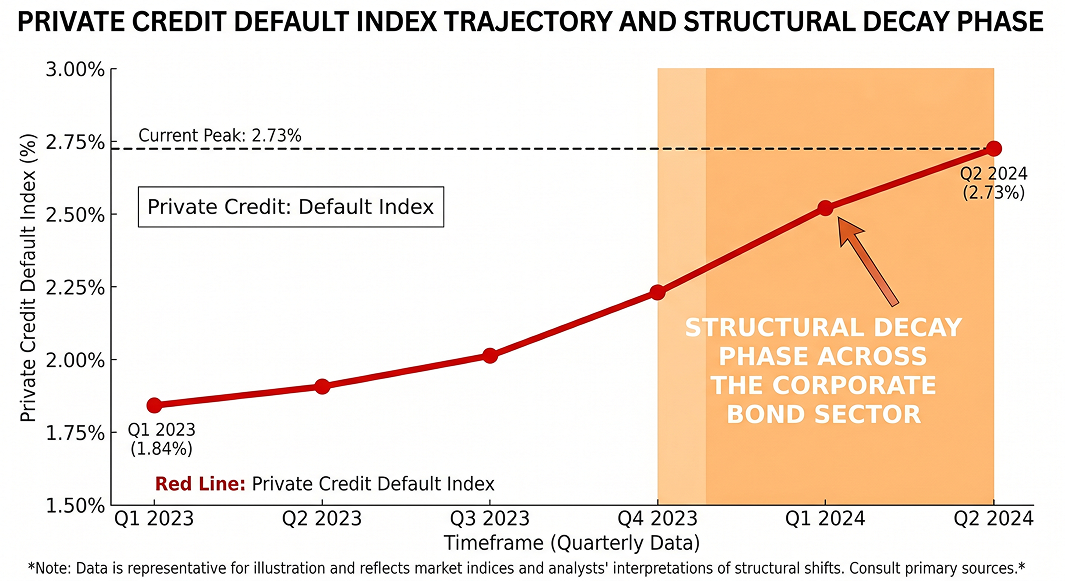

Let me pull back the boardroom curtain. The financial press is attempting to smooth over the edges, labeling the ongoing turmoil in the $2.1 trillion private credit market as a “healthy market correction.” In reality, it is a deep, structural decay. Severe underlying balance sheet damage is being masked by distressed debt exchanges and “payment-in-kind” (PIK) arrangements—accounting maneuvers designed purely to delay the day of reckoning.

The raw data speaks for itself. Proskauer’s Private Credit Default Index, which tracks hundreds of major mid-market loans worth $189.2 billion, climbed to 2.73% in the first quarter. Analysts at Morningstar DBRS recorded a staggering 78% jump in default events over the past year and expect this clip to hold steady.

Distressed debt exchanges accounted for 94% of all default-category downgrades over the last 12 months. In plain terms: corporations are not paying back their debts. They are simply restructuring timelines or paying their coupon obligations with more debt notes instead of hard cash. This is textbook balance sheet manipulation that only increases the long-term leverage strain on these entities. According to Moody’s, these exact distress maneuvers drove roughly 65% of all private credit defaults last year.

This contagion hits the broader market directly. U.S. banking institutions have extended nearly $300 billion in credit lines to private credit firms. Analysts at Morgan Stanley project that default rates across both the technology sector and private credit spaces will expand to 5.5% and 8% respectively. If you are holding popular high-yield business development companies (BDCs) like Ares Capital (ARCC), take note: analysts are already warning of significant redemption pressure if retail market sentiment turns cold.

Your monthly cash flow cannot depend on whether a fund manager chooses to release your capital. A true sovereign income model is built exclusively on assets you own outright. You open the positions, you manage the cash flow, and no institutional gatekeeper has the authority to freeze your liquidity.

.

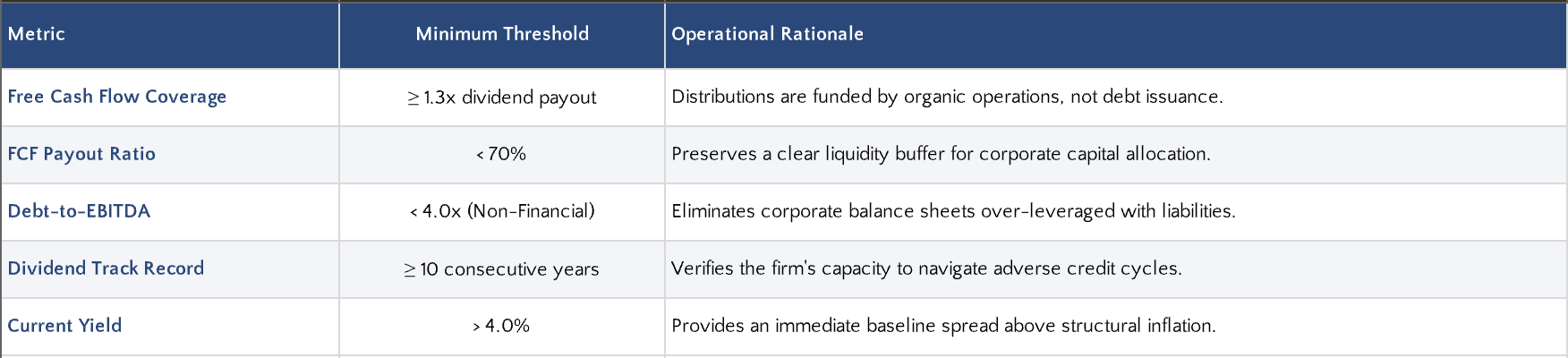

2. The Durability Filter: Separating Real Dividend Yield from Structural Traps

U.S. inflation continues to hold at a annualized rate of 2.6%. Every corporate CFO understands a fundamental rule that retail financial planners rarely mention: even a modest 2.5% inflation rate strips away 22% of a fixed income’s purchasing power over 10 years; over 20 years, those losses approach 40%. With non-discretionary costs like healthcare and shelter expanding at a faster clip, data shows that a typical retiring couple now requires hundreds of thousands of dollars just to secure basic medical coverage over their retirement horizon.

Against this backdrop, the S&P 500 yields a negligible 1%. Allocating $10,000 into a standard index-tracking ETF yields a trivial $100 per year. That is not an income stream; it is a statistical rounding error. To counter this, we isolate high-quality enterprises yielding above 4% that are explicitly insulated by robust free cash flow and conservative leverage metrics.

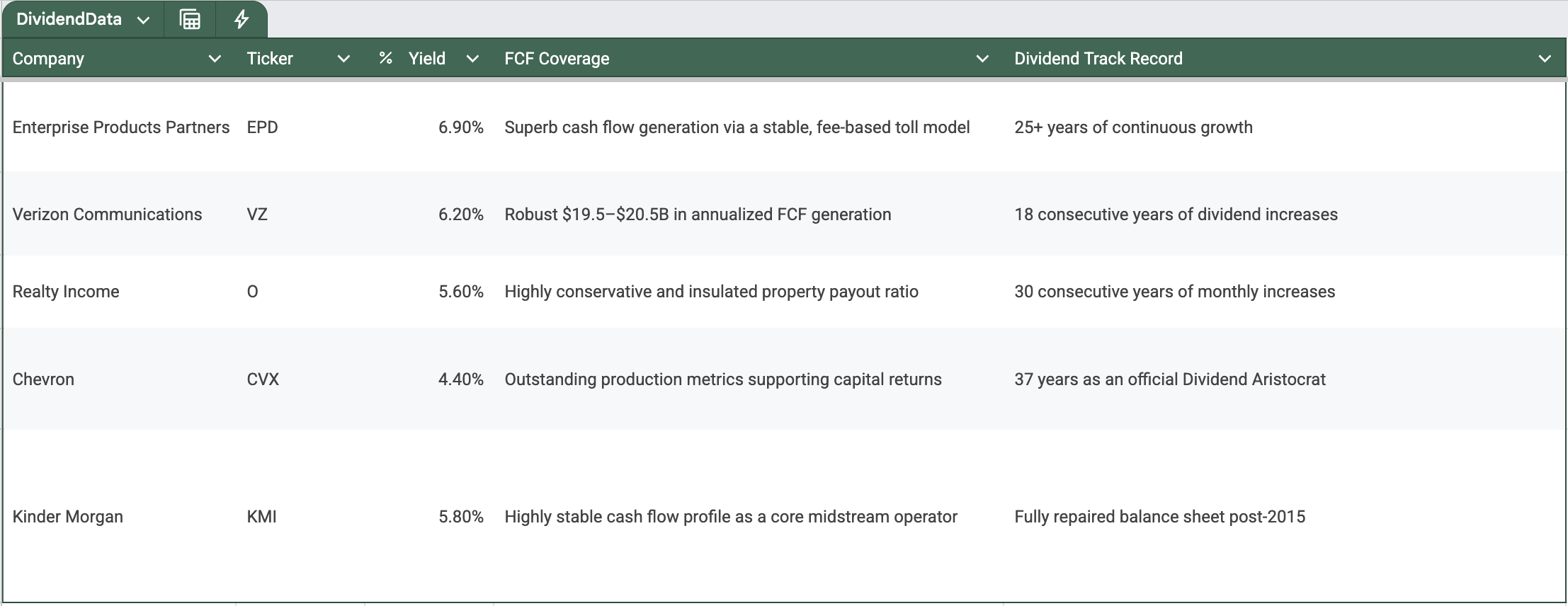

The following blue-chip equities currently meet these parameters:

Note what is intentionally absent from this index: any equity carrying a headline yield north of 10%. Double-digit yields are almost always structural value traps. They indicate that the equity price has collapsed because the market is pricing in an imminent dividend cut. Equities like Walgreens (8.2%) or Pfizer (7.0%) require deep structural restructurings before they warrant capital placement. Our operational rule is absolute: sustainable, verified free cash flow must always take priority over headline yield.

3. The Covered Call Overlay: Engineering Your Cash-Flow Engine

Securing fortress-grade dividend payers is simply the baseline. The covered call overlay serves as our primary yield enhancement vehicle. This mechanics converts a standard 5–7% dividend yield into a consistent 10%+ annual cash-flow stream. This is not speculative guesswork; it is the exact execution model deployed by institutional derivatives desks to systematically harvest premium from market volatility.

The mechanics are straightforward: you sell an out-of-the-money call option against equities you already own outright, immediately collecting the cash premium into your account. If the underlying stock price remains below your selected strike price at expiration, the option expires worthless. You retain your equity shares, pocket the corporate dividend, keep 100% of the option premium, and immediately write the next contract. The VettaFi Energy Covered Call Index demonstrates this mechanics at scale: overlaying systematic call options onto a 7% yielding equity basket captures an extra ~0.50% per month (~6% annualized), bringing total target yields to 10–11%.

Let’s look at the exact math mapped onto a $500,000 portfolio structure:

This yields a clean $4,417 per month deposited directly into your liquid account. There are no institutional gates from BlackRock, and no liquidity freezes from Blue Owl. Your capital remains within your own sovereign framework.

Operational Parameters for Option Execution:

- Strike Selection: Sell call options 3–5% out-of-the-money, targeting an options Delta within the 0.25–0.30 range. This parameters maintains sufficient equity upside exposure while maximizing the mathematical probability of the option expiring out-of-the-money.

- Expiration Horizon: Utilize short-duration contracts with a 30–45 day horizon. This represents the optimal acceleration curve for options time decay (Theta), working entirely in your favor as the net seller.

- Position Concentration: Limit any single equity position to a maximum of 8–10% of total portfolio value. Over-concentration in a single name is the silent killer of steady cash-flow strategies.

- Risk Mitigation (Rolling): If the underlying equity price tests your strike within 7 days of contract expiration, execute a rolling transaction—buy back the current option and sell a new contract one month out and at a higher strike. This captures more premium while protecting your shares and dividend access.

We run this overlay exclusively across large-cap, blue-chip enterprises with deep options liquidity chains: Enterprise Products, Verizon, Realty Income, and Chevron. These are infrastructure toll-road enterprises that generate billions in liquid cash flow. Capturing this premium is not a directional market bet; it is a systematic conversion of market volatility into a reliable monthly salary replacement.

4. The Allocation Blueprint and Sovereign Directive

The Federal Reserve maintains its benchmark interest rate target at 4.25%–4.50%, with interest-rate futures pricing in a high probability of methodical rate cuts as the broader labor market softens. As yields on government debt contract, institutional demand for high-quality equities yielding 5–8% will naturally intensify. Rate-sensitive equity sectors—specifically real estate investment trusts (REITs) and midstream utilities—are positioned to capture the strongest capital inflows.

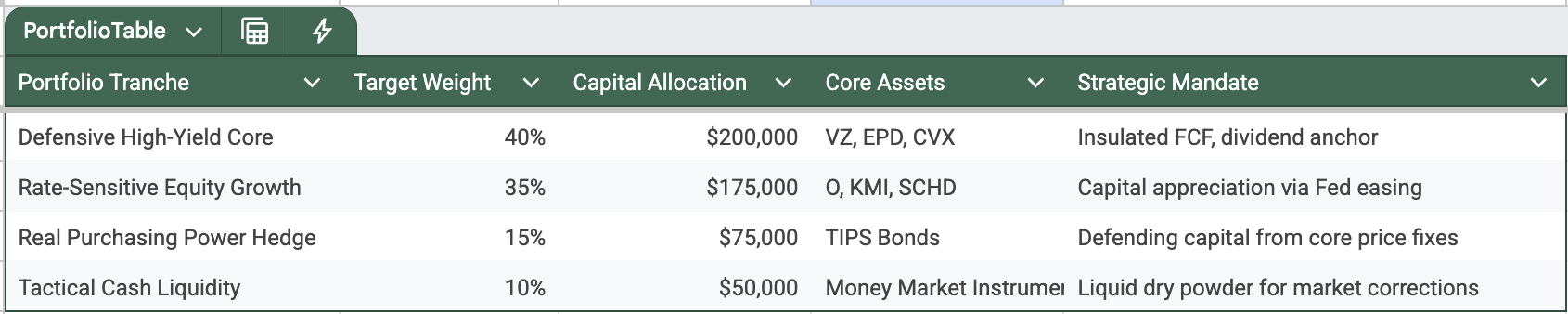

Sovereign Allocation Blueprint ($500,000 Reference Portfolio):

The covered call overlay is deployed across the Defensive Core and Rate-Sensitive tranches, routing $375,000 of working capital into setups that concurrently generate corporate dividends and short-duration options premiums. The inflation-hedged TIPS allocation acts as a long-term buffer to insulate your principal, as consumer prices have structurally set a higher baseline. The tactical cash reserve has a single mandate: stand ready to aggressively acquire shares of these fortress companies during periods of credit-driven market corrections.

Operational Risk Guardrails:

- Audit free cash flow metrics quarterly. If any underlying holding drops below a 1.3x FCF dividend coverage threshold, immediately suspend option writing on that position and initiate a structural position review.

- Monitor macro default rates. If the headline Fitch default rate crosses 7.5%, systematically reallocate 10% from rate-sensitive equities into your tactical cash reserve.

- Maintain absolute yield discipline. Never chase double-digit headline distributions. Outsized yields are a market signal of profound structural balance sheet issues, not an investment opportunity.

The Sovereign Directive: Deep analytical rigor—the ability to dissect a corporate balance sheet, spot hidden liabilities behind glossy investor presentations, and distinguish true free cash flow from reporting manipulation—is your greatest weapon in this market environment.

The private credit arena is experiencing real cracks. Elite multi-billion-dollar funds are enforcing redemption gates on investors who placed their faith in institutional marketing. The broader S&P 500 pays a nominal 1%. The legacy financial architecture was never engineered to fund your personal sovereignty; it was designed to extract management fees from your capital.

Your counter-strategy is a calculated, math-driven execution framework: $4,417 per month generated by high-quality assets held in your direct custody, enhanced by options premiums under your total control. I allocate my own capital alongside the exact frameworks detailed in this brief. This is not academic theory; it is daily capital execution. Build the portfolio architecture, write the contracts, and collect your cash flow. You are no longer a line-item corporate liability. You are an Individual Sovereign—and the market is open.

The Corporate Debt Landmine Report: Covered Calls on Fortress Balance Sheets

The S&P 500 yields just 1%. Our covered call overlay targets 10%+ annual income.