I spent twenty-two years inside executive boardroom strategy sessions. The big capital allocations always happened behind closed doors, only hitting the quarterly earnings calls months after the money had already moved. What is quietly unfolding in Tokyo right now isn’t a flash-in-the-pan media headline; it is a fundamental rewiring of Asia’s financial plumbing.

This operational shift spans three layers simultaneously: regulatory frameworks, institutional banking networks, and public exchange architectures. Japan’s primary financial regulator, its three largest megabanks, and the ruling political party have all synchronized their entry into the digital asset landscape this quarter. Such a coordinated maneuver indicates a systemic deployment of institutional infrastructure.

For any independent investor focused on generating a consistent cash-flow stream from the public markets, this structural migration demands full attention. This briefing breaks down the verified data, details the precise scale of the market opening, and outlines a clear framework to position your capital ahead of the institutional wave. Our mandate is to outmaneuver large-scale market participants by anchoring our capital to verifiable financial metrics.

1. The Regulatory Playbook: Exposing the 20% Tax Catalyst

Let me be direct about the regulatory architecture Japan’s Financial Services Agency (FSA) is putting together. The FSA has formally proposed moving 105 digital assets under the strict legal jurisdiction that governs standard equities. This isn’t a minor administrative tweak; it places these assets into the exact same regulatory lane as large-cap stocks and corporate bonds.

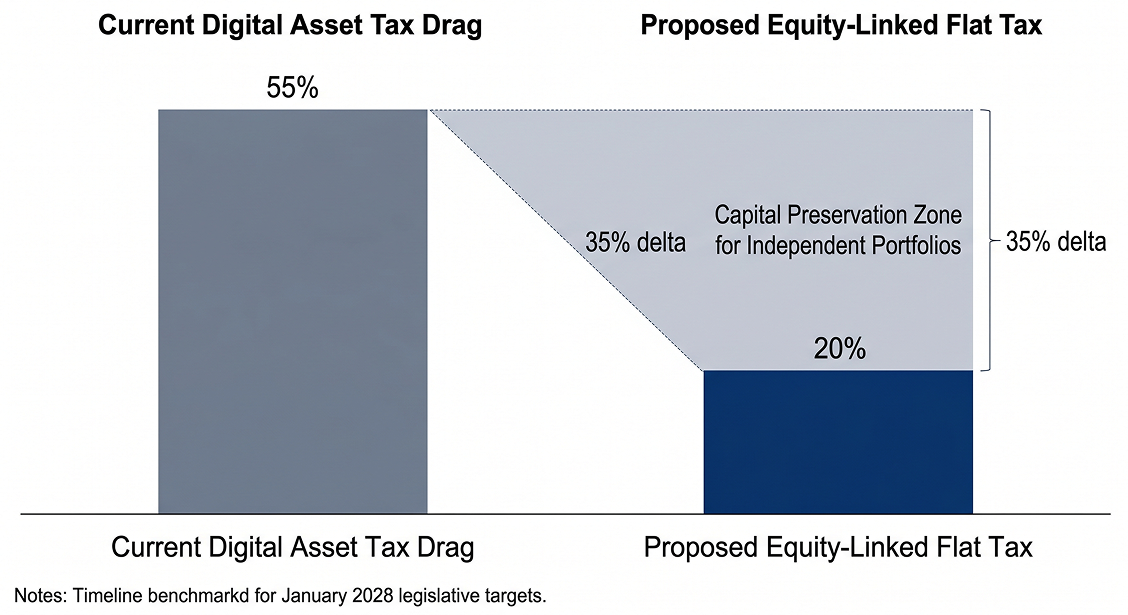

The underlying math represents a massive reduction in administrative drag. Currently, Japan taxes these gains as miscellaneous income at rates reaching up to 55%. The new structural plan collapses that down to a flat 20% rate to match standard stock distributions. For a self-directed portfolio, that represents a massive 35-point reduction in tax friction. That is a balance sheet event.

However, proper position sizing requires assessing the legislative timeline. The bill has been officially submitted to the Diet, but it has not yet passed into law. The targeted execution date for the 20% flat rate and crypto ETF access is set for January 2028.

I never allocate capital based on assumptions. I trade on verified catalysts with clear timelines. This path is heavily backed by the FSA, the ruling Liberal Democratic Party (LDP), and the exchange operators. Concurrently, as of June 1, 2026—today—foreign-issued stablecoins like USDC are legally cleared to circulate within Japan under strict reserve mandates requiring 100% backing and a complete ban on fractional lending

.

2. The Banking Infrastructure: Megabanks and the Cross-Border Pipeline

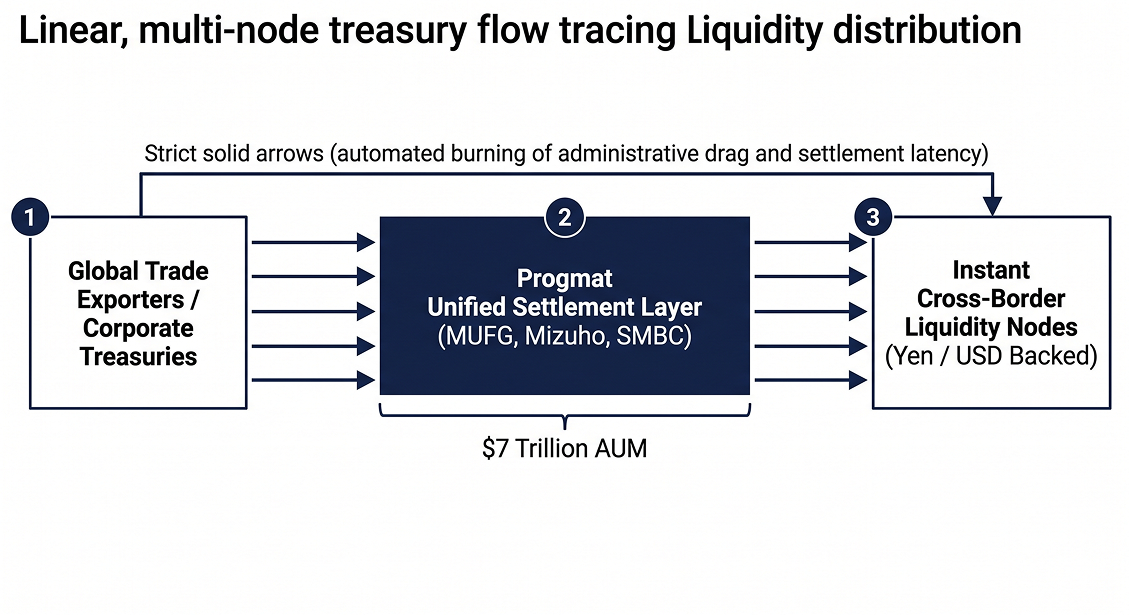

In my years managing corporate balance sheets, one operational signal always carried the most weight: real capital commitment. Press releases are entirely meaningless unless they are backed by institutional infrastructure. Japan’s three largest financial institutions—MUFG, Mizuho, and SMBC—have officially mobilized a unified stablecoin settlement pilot utilizing the institutional Progmat platform.

This isn’t an isolated sandbox experiment; it specifically targets yen-backed stablecoins for large-scale domestic and cross-border corporate treasury settlements. The banking group is simultaneously testing a USD-denominated variant to streamline global trade flows for major industrial exporters. When three banking entities holding over $7 trillion in combined assets move in lockstep, the inefficiencies of legacy settlement layers are being systematically engineered out of the system.

The true scale of this infrastructure shift is clearly visible in the macroeconomic data. The broader Asian market processed $12.5 trillion in stablecoin settlement volume over the past year—a sharp 67% increase from the prior period. This growth isn’t driven by retail speculation; it is driven by corporate treasury optimization.

Furthermore, the European Central Bank (ECB) confirmed on June 1 that this accelerating global stablecoin layer is actively cementing dollar dominance through structural network effects. In tandem, major regional asset managers like SBI Holdings, Rakuten, and Nomura are building regulated investment trusts to capture this institutional flow

.

3. The Active Management Deficit: Capitalizing on the ETF Gap

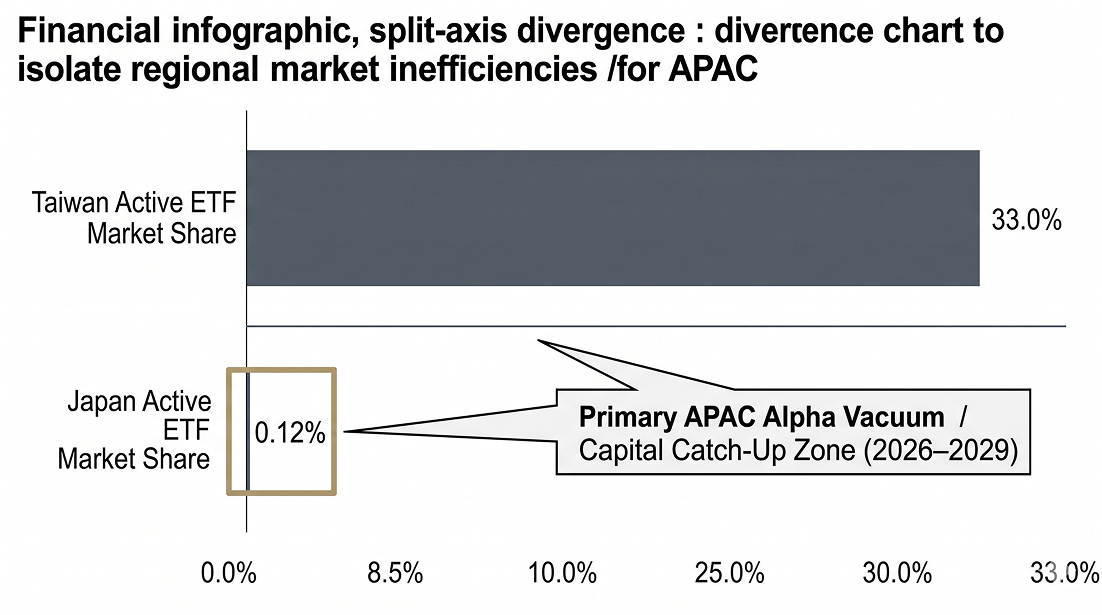

Here is the structural asymmetry that should stop you cold. The global ETF market currently commands $19.9 trillion in assets across more than 14,500 listed products. The Asia-Pacific region is expanding at a 25% compound annual growth rate (CAGR) over the last decade, handily outpacing the U.S. growth rate of 20%. Japan leads the entire region in total asset volume, yet its active ETF market share stands at a microscopic 0.12%. For perspective, Taiwan’s active share sits at 33%.

This massive delta is not an operational failure; it is the single largest growth opening in the APAC region over the next five years. Active yield-generation funds, macro rotation vehicles, and institutional covered call structures are primed to flood this vacuum as Japanese portfolios modernize.

Tokyo Stock Exchange CEO Hiromi Yamaji confirmed that the exchange is actively laying the operational groundwork for crypto ETF listings. The target implementation window is focused on a planned update to the Investment Trust Act.

When the head of a major global stock exchange, the primary financial regulator, and the ruling political party all signal structural readiness, the long-term direction is clear. BlackRock’s IBIT has already proved this wrapper works at scale, capturing nearly $100 billion in assets under management. As Japan’s regulatory framework matures toward the 2028 window, this emerging pipeline creates a highly predictable multi-year capital migration

.

4. The Sovereign Directive: Operational Capital Framework

Let’s organize these macroeconomic catalysts into an actionable, risk-mitigated execution framework:

- Active ETF Asymmetry: Monitor large-cap, APAC-weighted funds as the active management gap inevitably compresses toward standard global averages. The influx of yield-focused strategies—including covered calls and cash-secured puts—into the Japanese exchange system fits perfectly into an independent cash-flow model.

- Infrastructure Nodes: The $12.5 trillion regional stablecoin layer is a permanent utility, not a speculative trend. The commercial entities operating this plumbing—payment tech firms, enterprise custodians, and core exchange operators—hold the true operational leverage.

- Tax Migration Positioning: A 35-point reduction in asset class friction will trigger massive reallocations from institutional desks. Position your portfolio along the path of the catalyst, not after the final media confirmation.

- Strict Risk Parameters: Never substitute analysis with enthusiasm. The proposed regulatory changes are pending final legislative passage. Position sizes must reflect that political and legislative timelines always carry structural execution risk.

When the institutional machine decided my twenty-two years of corporate execution was simply an expensive line item and handed me a pink slip, I realized a fundamental truth: the system was never engineered to protect your personal capital. A $19.9 trillion global market gap isn’t just an abstract data point—it is raw material for you to build your own financial autonomy.

Japan isn’t just opening up to digital assets; it is building the heavily regulated, tax-efficient corporate rails that convert volatile assets into a predictable, defensible, and fully controlled income stream. The establishment never intended to offer you a seat at this table. Build your own.

The Yen Stablecoin Offensive: A Sovereign Capital Briefing You Cannot Ignore

Three megabanks, one stablecoin pilot, and a $12.5T settlement layer you need to understand.